When it comes to planning for retirement, the focus has traditionally been on accumulation (saving and investing money for retirement) vs. decumulation (drawing down one’s accumulated retirement savings in retirement). So, it’s not surprising that retirees may feel uncertain or uneasy about how much they can safely withdraw and spend from their accumulated savings once retirement arrives.

As opposed to taking withdrawals from savings to meet spending needs, is there a more optimal way to create income from savings to help support more worry-free retirement spending — particularly for people who may be behaviorally resistant to spending down their savings? Two prominent retirement income experts believe there is — and it involves converting more of one’s accumulated savings into lifetime income through financial products such as annuities.

In their work for the Alliance for Lifetime Income’s Retirement Income Institute, fellows David Blanchett and Michael Finke find that retirees are reluctant to spend their retirement savings. Instead, retirees spend significantly more from their sources of lifetime income (that is, Social Security, pensions, and/or annuities) than they do from their savings in IRAs and other retirement accounts.

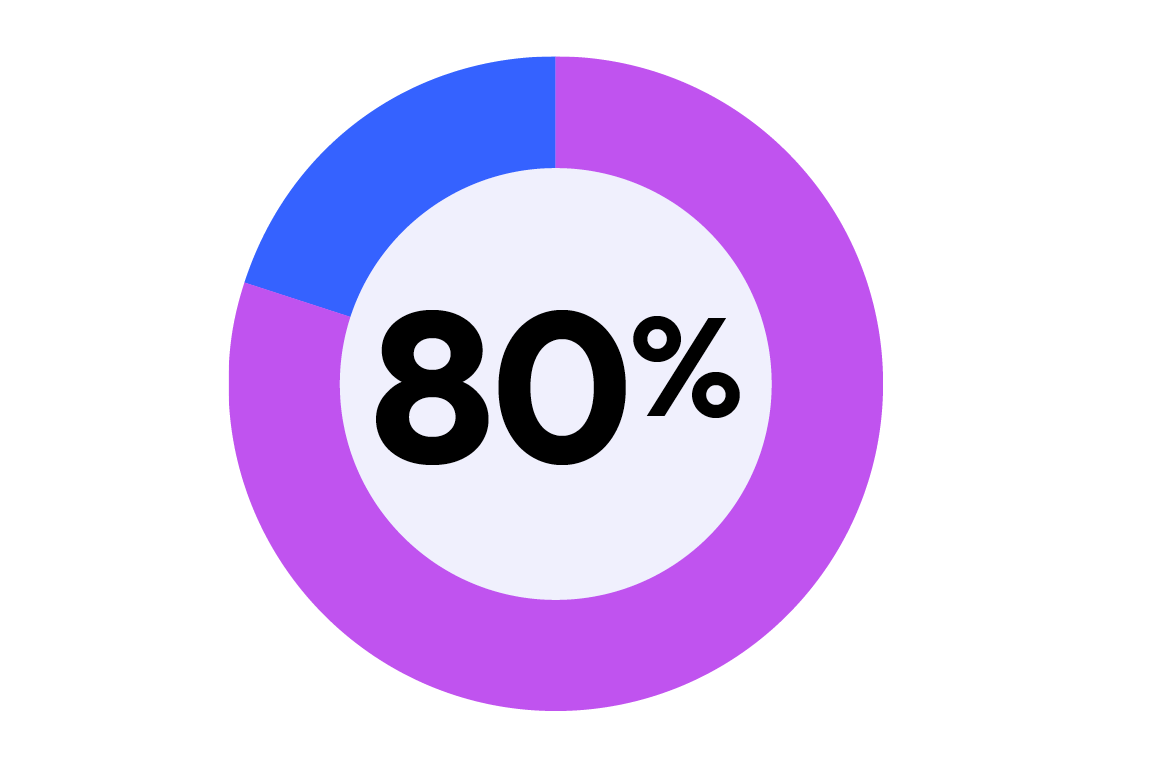

Overall, their analysis suggests that converting a portion of retirement savings into lifetime income, through products such as annuities, could increase retirement spending significantly, especially for married households. The analysis clearly demonstrates that households spend differently across sources of wealth. Retirees spend a much higher percentage of their lifetime income (about 80%) and spend about half the amount that they could safely spend from other sources.

So, what may be driving some retirees to hold on to their retirement savings so tightly? The authors believe one potential explanation for lower than optimal spending is the general dislike of spending down wealth during retirement. Or put another way, the fear that every dollar of savings spent in retirement brings one that much closer to running out of money. People tend to view money held in savings accounts differently than wealth held in the form of income. Plus, there’s the challenge of decumulation complexity.

According to the Alliance study, estimating how much income can be withdrawn from investments is far more complex than receiving a monthly pension payment. Retirees face a number of complicating factors, including potentially limited financial knowledge, an unknown lifespan and the variety of financial resources they must consider, such as Social Security, and investment assets inside and outside of retirement accounts they may hold.

Recent research from Corebridge Financial further underscores the anxiety people feel about withdrawing money from their savings in retirement. Thirty-nine percent of retirees say they feel anxious about not having saved enough money to last throughout retirement or are worried they may be spending too much when they withdraw money and see their account values decline.3

To better understand how people 65 and older are spending money, the study’s authors analyzed data from the Health and Retirement Study, which is an ongoing nationally representative survey of approximately 20,000 Americans over the age of 50. The study is supported by the Social Security Administration and National Institute on Aging. In the Alliance study, two broad categories of available financial resources or assets were considered by Blanchett and Finke — income and savings:

- Income was separated into three groups: lifetime income (Social Security, pensions, and annuity income), earnings (wages and salaries for those who have not fully retired), and capital income (which includes income from businesses, rental property, dividends and interest, and trust funds or royalties).

- Savings were broken into qualified (defined contribution balances, IRAs, etc.) and non-qualified monies held in taxable accounts.

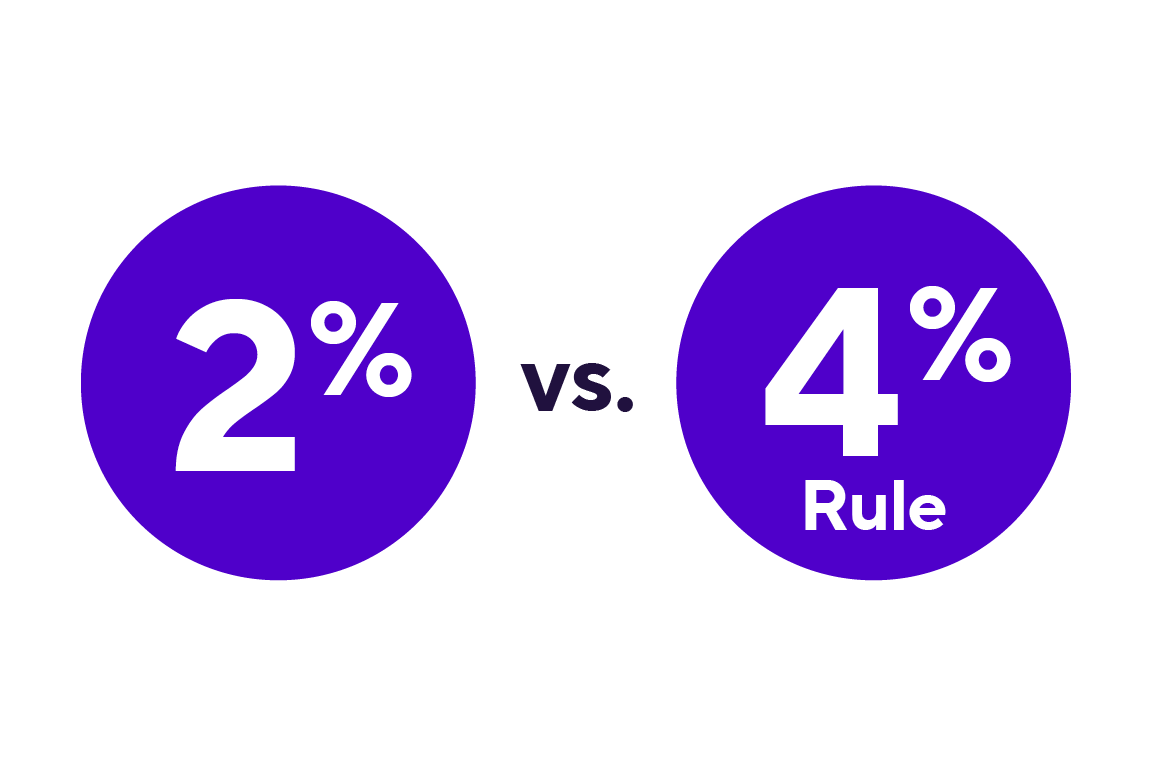

Their analysis found much higher spending rates from lifetime income sources than from wages or capital income. Roughly 80% of lifetime income is spent, while less than half of wage income and capital income are spent. In addition, 65-year-old couples were found to be spending just 2% of their savings, which is roughly half of the commonly cited “4% rule.”

80% of lifetime income is spent, while less than half of wage income and capital income are spent

65-year-old couples studied spent only 2% from savings, roughly half of the commonly used 4% rule

65-year-old couples studied spent only 2% from savings, roughly half of the commonly used 4% rule

“Unless people purposefully want to leave behind a large bequest when they die, many retirees are denying themselves the opportunity to enjoy life by spending more of their savings,” said study co-author Blanchett, Head of Retirement Research at PGIM DC Solutions.

“I don’t think people purposefully want to hoard their savings; they are just finding it difficult to view savings as a potential form of retirement income,” added Finke, Professor and Frank M. Engle Chair of Economic Security Research at the American College of Financial Services. “They are able to make that adjustment when they receive annuity and RMD payments, so there is a path to getting over this behavioral barrier.”

Interestingly, with respect to RMDs (Required Minimum Distributions), the study found that retirees spend a higher rate of their savings after the federal government requires such distributions from their retirement savings accounts. Retirees seem to view the forced asset distribution as income and spend it at a higher rate than they spend from other savings. RMDs are the minimum amounts people must withdraw annually starting at age 73 from qualified investment accounts to avoid penalties to the IRS. Accounts subject to RMDs include traditional IRAs, SEP IRAs, and most employer-sponsored retirement plans like 401(k)s and 403(b)s.

As the study noted, lifetime income sources such as Social Security, pensions and annuities remove both the uncertainty of longevity and the complexity of estimating a safe withdrawal rate from investment assets. Prior work from Blanchett and Finke found retirees spend far more when they hold a larger share of total wealth in lifetime income than if they hold the wealth in investment assets.4

Their latest research suggests that retirees who are behaviorally resistant to spending down savings may better achieve their lifestyle goals by increasing the share of wealth allocated to financial products that offer lifetime income, such as annuities. The study further noted that annuities not only can reduce the risk of an unknown lifespan, but they can also allow retirees to spend their savings without the discomfort generated by seeing one’s nest egg get smaller.*

“...retirees who are behaviorally resistant to spending down savings may better achieve their lifestyle goals by increasing the share of wealth allocated to financial products that offer lifetime income, such as annuities.”

To learn more about annuities and protected lifetime income, talk to your financial professional today. You can also learn more about annuities with our Fresh Look at Annuities series of educational articles.

*Annuities can provide guaranteed lifetime income through annuitization, a process that converts the contract value, or principal, into a series of guaranteed income payments. Once a contract has been annuitized, the annuity owner no longer has access to the contract value or principal. Alternatively, for those seeking more flexibility, many of today’s annuities offer income benefits, such as guaranteed lifetime withdrawal benefits and guaranteed living benefit riders. These income benefits provide guaranteed lifetime income and the annuity owner retains access to their contract value. Annuity income benefits may be standard or optional. Additional fees, age restrictions, withdrawal parameters and other limitations apply. Though some annuities with an income benefit have an income base or withdrawal benefit base that generally remains steady (or can potentially increase depending on the terms of the benefit), an annuity’s contract value will decline due to fees and withdrawals or income taken within the terms of the rider or benefit, and excess withdrawals may terminate the income benefit. There is no guarantee that income will keep pace with or protect against inflation.

1Alliance for Lifetime Income Retirement Income Institute, “Retirees spend their lifetime income, rather than savings,” press release, April 8, 2025.

2David Blanchett and Michael Finke, “Research Paper: Retirees Spend Lifetime Income, Not Savings,” Alliance for Lifetime Income Retirement Income Institute, April 2025.

32025 Corebridge Financial Living and Funding Longer Lives Study.

4David Blanchett and Michael Finke, “Guaranteed Income: A License to Spend,” Alliance for Lifetime Income Retirement Income Institute, May 2024.

RO #5191272