Americans are living longer. And while that's great news, it’s important to understand how longevity changes the way we prepare for, transition to and live in retirement. To better understand how well people understand longevity risk and opportunity, Corebridge Financial and the Longevity Project conducted research to explore how Americans ages 18+ feel about their potential to live to 100 and their ability to plan for longevity.1

Overview:

In our latest study, we find that Americans express guarded optimism about their longevity — and they have very real concerns about how later life will be lived, pointing to health, financial and quality of life worries. Our study on living and funding longer lives provides direction on the steps that can be taken to help individuals address common concerns, achieve their goals, and fully live and fund their longer lives.

Findings at-a-glance:

- Half of Americans (50%) believe they could reach age 100, with Gen Z and millennials the most positive of the generations, at 57% and 49%, respectively. Family longevity plays the biggest role in longevity optimism — those with family members age 95+ are the most likely to feel they could reach age 100.

- There is a clear disconnect, however, between longevity expectation and retirement planning — half of non-retired respondents are only planning for 20 years or less in retirement, even though the majority don’t plan to work beyond their sixties, and many expect to retire before age 65.

- Physical well-being, healthcare costs and financial security are top longevity concerns, emphasizing the crucial interplay of health and wealth in retirement.

- Americans report high levels of stress generally, but particularly around financial security. Many hope to take action in the next year to reduce their financial stress.

- Securing lifetime income in addition to Social Security is a high priority — and can even impact current levels of happiness and well-being.

There is an understanding among the general population that people are living longer, with 50% of Americans believing it's possible they could live to see age 100. This belief is even higher among younger respondents — 54% of Americans ages 18-34 say it's possible, compared to only 45% of those age 50-64. Surprisingly, men are more likely than women to believe in their own longevity, even though women outlive men by 5.3 years.2

Notably, family longevity plays a role in longevity optimism — 67% of people who have centenarian family members feels it's possible they could achieve a 100-year life.

; quality of life (86%); serious health problems (85%); cognitive decline (84%); losing independence (83%); healthcare costs (82%); being a burden on family (74%); and running out of money (69%). What do Americans fear more: running out of money or death? 62% say running out of money. 38% say death.")

; quality of life (86%); serious health problems (85%); cognitive decline (84%); losing independence (83%); healthcare costs (82%); being a burden on family (74%); and running out of money (69%). What do Americans fear more: running out of money or death? 62% say running out of money. 38% say death.")

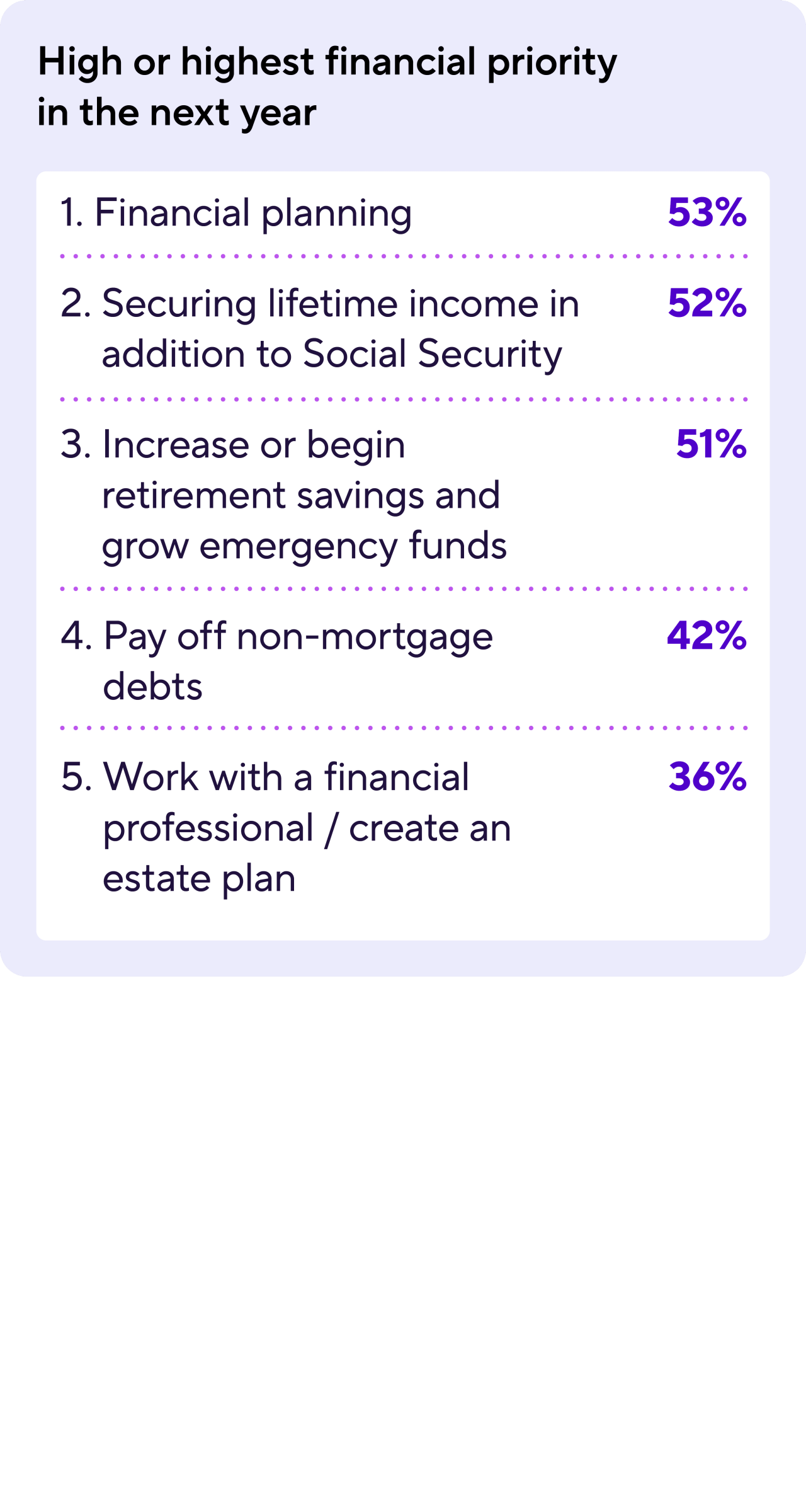

; increase or begin retirement savings (88%); secure lifetime income in addition to Social Security (83%); start or grow an emergency fund (82%); pay off non-mortgage debt (75%); create an estate plan (65%), and work with a financial professional (64%).")

; increase or begin retirement savings (88%); secure lifetime income in addition to Social Security (83%); start or grow an emergency fund (82%); pay off non-mortgage debt (75%); create an estate plan (65%), and work with a financial professional (64%).")

; plan for a successful financial future (53% vs. 32%); manage their retirement money to provide income for life (48% vs. 31%); not outlive their money (35% vs. 25%); and pay for unexpected expenses (47% vs. 30%).")

; plan for a successful financial future (53% vs. 32%); manage their retirement money to provide income for life (48% vs. 31%); not outlive their money (35% vs. 25%); and pay for unexpected expenses (47% vs. 30%).")

. Annuity owners are also more likely than non-annuity owners to say that when it comes to their current level of financial stress, they're not too stressed (52% vs. 41%).")

. Annuity owners are also more likely than non-annuity owners to say that when it comes to their current level of financial stress, they're not too stressed (52% vs. 41%).")