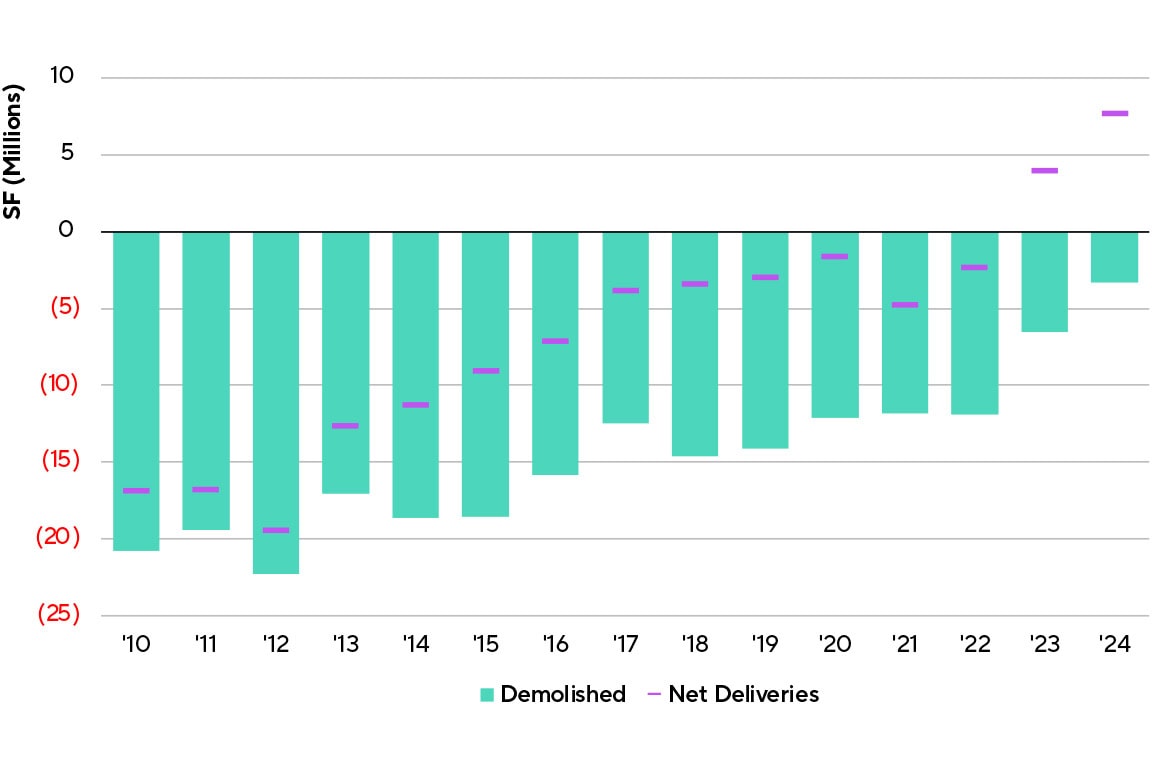

Developers, riding the pandemic-induced logistics boom, appear to have overestimated the demand for such assets as large companies like Amazon scaled back leasing and acquisitions. As a result, vacancy in assets over 150,000 square feet today is now nearly double that of the smaller industrial properties where demand remains strong. The individual suites within these smaller properties - specifically those under 50,000 square feet - have also seen rents grow by over 40% since 2020, compared to around 30% for the broader market. These and other market dynamics today give small bay light industrial advantages over other sectors and position the sub-class as one of the most compelling real estate investment opportunities in 2025.

Market dynamics for small bay industrial properties

Demand and scarcity

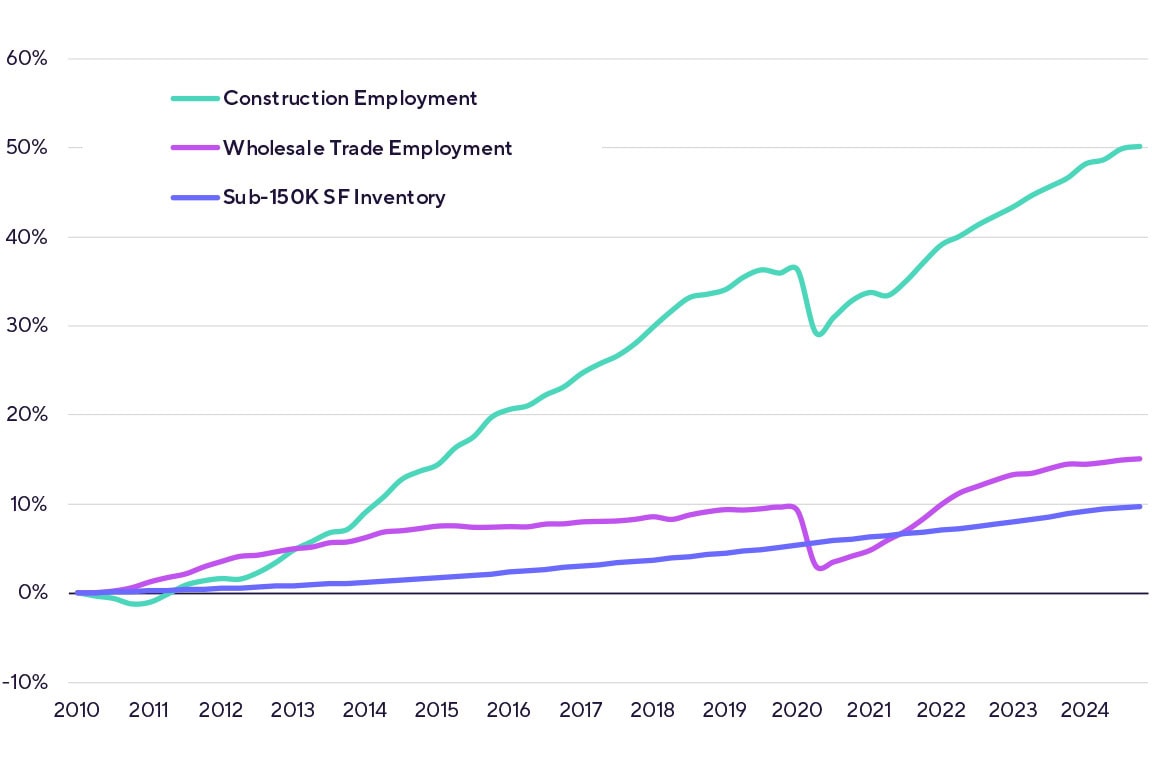

An examination of U.S. industrial markets reveals that the strongest demand in today’s market is concentrated in smaller, multi-tenant, infill industrial and warehouse properties. These assets tend to cater to a diverse range of businesses making them more resilient to economic downturns. While large firms can consolidate and reduce their real estate footprint in uncertain times, smaller businesses do not have the luxury of forgoing the essential space required for daily operations.

Moreover, employment in industries that heavily rely on small bay properties such as construction and wholesale trade has outpaced the available inventory. Small businesses, the primary tenant base for this asset class, have also benefited in recent years from supportive government programs and more accessible bank lending standards.

Exhibit 1:

Cumulative growth of small bay industrial stock and key industry employment

Source: St. Louis Federal Reserve, CoStar

Compounding this demand surge is a significant supply constraint. Rising construction costs following the pandemic have made new light industrial development largely cost-prohibitive, further tightening availability. The new warehouse construction cost index shows a 44% increase in development costs from the beginning of pandemic to today. The 90 million square feet of small bay industrial space currently under construction nationwide represents just 0.5% of existing stock, a figure that has continued to decline since interest rates moved off historic lows in early 2022.

Exhibit 2:

New warehouse construction cost index

Source: St. Louis Federal Reserve

“Industrial construction projects of all stripes are significantly more expensive to build now than in previous years. Costs remained stable by YE 2024, yet a variety of headwinds including rebuilding efforts after devastating California wildfires, tariff uncertainty, and immigration policies could cause costs to stay elevated or move up in the short to mid term” - Newmark Research