You are: individual

How is SECURE 2.0 relevant to you?

Select one of the options below to learn more.

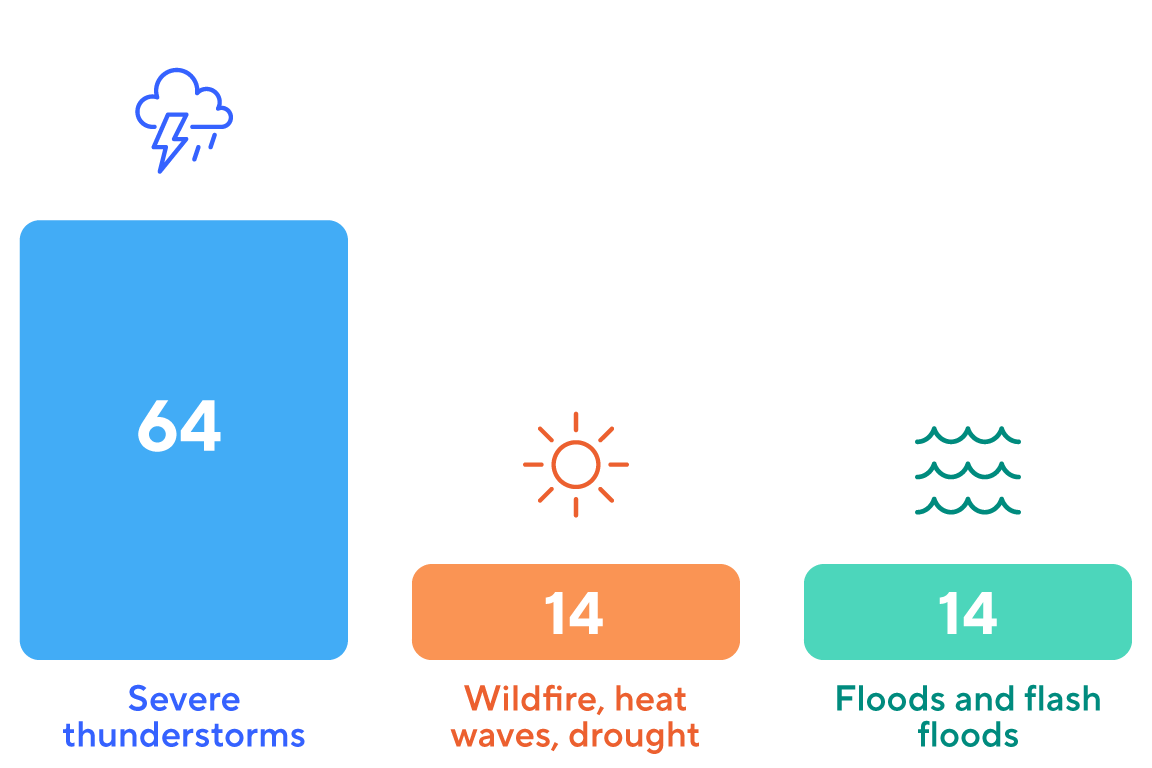

Natural disasters create an immediate hardship

Source: The Wall Street Journal, “Americans Tap 401(k) Plans After Hurricanes and Natural Disasters,”

Oct. 4, 2022

Source: statista.com, Natural disasters in the U.S. – Statistics & Facts, Nov. 29, 2022.

- The maximum distribution is $22,000 per disaster aggregated across all employer-sponsored and individual retirement plans.

- The maximum loan is the lesser of $100,000 or 100% of the vested account balance. Plans can also suspend loan repayments for up to one year (requires loan extension).

- In addition, the QDRD must be made within 179 days after the later of the first day of the incident period or the date of the disaster declaration (for example, for disasters that occurred between January 26, 2021, and December 29, 2022, the deadline was June 27, 2023).

There are some things money can’t buy

- Repayment of natural disaster distributions will be treated as if the distribution was an eligible rollover distribution and as having satisfied the requirements for a 60-day rollover—if the plan accepts rollovers.

- In addition, participants who take QDRD can repay the distribution regardless of their eligibility to contribute to the plan. However, repayments of distributions for terminal illness can only be made if the participant is otherwise eligible to contribute to the plan.

SECURE 2.0 Provisions Effective in 2024 and Beyond

- $10,000 (indexed for inflation); or

- 50% of their vested account balance.

- Individuals can self-certify that they are experiencing an unforeseeable and immediate financial need to avoid the 10% early withdrawal penalty.

- These distributions are limited to one per calendar year.

- No other emergency distributions can be taken in the following three years—unless the original distribution is repaid, or future distributions exceed the amount of the previous emergency distribution.

- with compensation less than $150,000;

- who do not own more than a 5% interest in the company; and

- who were not in the top 20% of employees when ranked by compensation.

Another option to fund long-term care

Source: Genworth, Cost of Care Survey, 2021

- Long-term care premium statement (showing premiums owed) that includes the name and tax identification of the insurance company

- A statement that the coverage is certified long-term care insurance

- Proof that the participant is the owner of the policy or the relationship of the covered person to the plan participant (if a spouse, for example)

1 Source: Primerica and Change Research Fact Sheet, Q4 U.S. Middle-Income Financial Security Monitor, January 2023.

2 Source: Debt.org, Hospice Costs & End-of-Life Options, Oct. 25, 2021.

3 Source: National Coalition Against Domestic Violence (2020). Domestic violence.

4 Source: National Domestic Violence Hotline, Understand Relationship Abuse.

5 Source: Bankrate.com, Bankrate’s 2023 annual emergency savings report.

6 Source: Singlecare.com, Long-term care statistics 2022.