Every person eligible for Social Security has an important question to answer – When should I start taking payments?

What about you? Have you thought about what you will do when that time comes? Have you decided whether you’ll take the payments right away or do you think it’s better to wait?

As you consider your answer, let’s explore several questions that can help provide more clarity.

Are you in good health?

While none of us has a crystal ball to reveal how long we’ll live, personal health history and family health history may provide key insight. For example, how long did your parents or grandparents live? If you expect to live a long life, you might decide it’s better to wait and get a higher monthly benefit rather than taking a smaller monthly amount sooner. On the other hand, if you aren’t in the best health – or if your parents or siblings have a history of poor health or longevity – taking benefits early might be a smart decision.

Do you have other sources you can initially draw on for retirement income?

Delaying payments often makes sense if you're in good health, but it might also be a smart choice if you don’t need Social Security payments to make ends meet in the early years of your retirement. The logic here is that if there are no urgent financial demands and you have sufficient savings or income to cover your expenses, you might consider delaying your benefits to receive a higher lifetime monthly payout. Conversely, if you have immediate financial needs that can’t be covered by savings and/or earnings, it might be smart to take payments earlier.

Do you have a spouse?

Deciding when to take Social Security benefits is often thought of as an individual decision. While that’s true, your choice can also have an impact beyond just your own finances during retirement. This is especially true for those who are married. So, before deciding when to file, consider what your decision could mean for your spouse. Or better yet, work together. Coordination between spouses can help maximize household benefits. For example, a lower-earning spouse might claim earlier, while the higher-earning spouse could delay benefits to increase the delayed retirement credits and potentially enhance the survivor benefit.

Will you continue working?

If you haven’t reached Full Retirement Age1 – and are still earning income – be sure to consider the impact of those earnings on your Social Security payments, as some of your benefits may be withheld. The Social Security Administration reduces benefits for those younger than Full Retirement Age or in the year they reach Full Retirement Age when annual earnings from work exceed a certain limit. Note, however, that if you’re working and you are older than your Full Retirement Age, there is no reduction in benefits. Keep in mind, if some of your benefits are withheld because of work, your benefits will be increased starting at Full Retirement Age to take into account those months in which benefits were withheld.

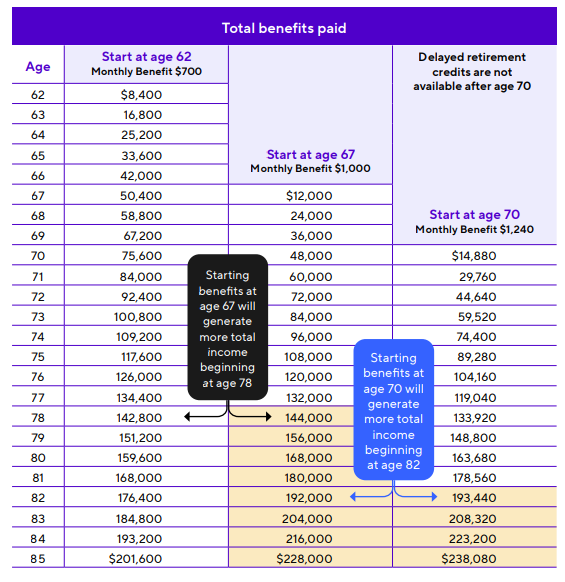

What is my break-even point?

Although waiting to take Social Security benefits brings a larger monthly payout, it also means you’ll receive fewer payments over the course of your life. With that in mind, it’s important to find the age at which the total amount of money you’d receive if you filed later equals the total amount of money you may receive if you file early. This is called your break-even point.

Said another way, if claiming at 62 – for example – gives you $700 per month, and claiming at 67 gives you $1,000 per month, calculate how many years it will take at the higher payment to make up for not taking the lower payment earlier. Having this figure – and a solid knowledge of the other factors like health, family longevity, wealth and marriage status – can help you determine if it makes sense to start your payments right away or to delay until a future date.

Here's a hypothetical example that shows total benefits paid through three common starting ages. The example assumes a $1,000 monthly benefit is available at Full Retirement Age of 67. Amounts shown do not reflect any cost-of-living adjustments.2

Have you talked to a financial professional about Social Security?

Ultimately, there is no single answer as to when to file for benefits since everyone enters retirement with a unique set of personal circumstances, financial needs and future expectations. While the questions posed here provide a starting point in your decision-making process, having a trusted financial professional by your side can help make sure your approach is the best one for your specific situation.

To that point, consider recent Corebridge research3 that reveals those who work with a financial professional are significantly more likely to feel confident in their ability to plan for a successful future than those who don't (53% vs. 32%).

1 Full Retirement Age is the age when you qualify for 100% of your Social Security benefits (known as your Primary Insurance Amount). Your Full Retirement Age is based on your year of birth. If you were born in 1960 or later, your Full Retirement Age is 67.

2 Note: Social Security benefits are adjusted each year to reflect the increase, if any, in the cost of living as measured by the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

3 Corebridge Financial 2025 Retirement and Longevity Survey.

This material is general in nature, was developed for educational use only, and is not intended to provide financial, legal, fiduciary, accounting or tax advice, nor is it intended to make any recommendations. Applicable laws and regulations are complex and subject to change. Please consult with your financial professional regarding your situation. For legal, accounting or tax advice consult the appropriate professional.