A look back at the market

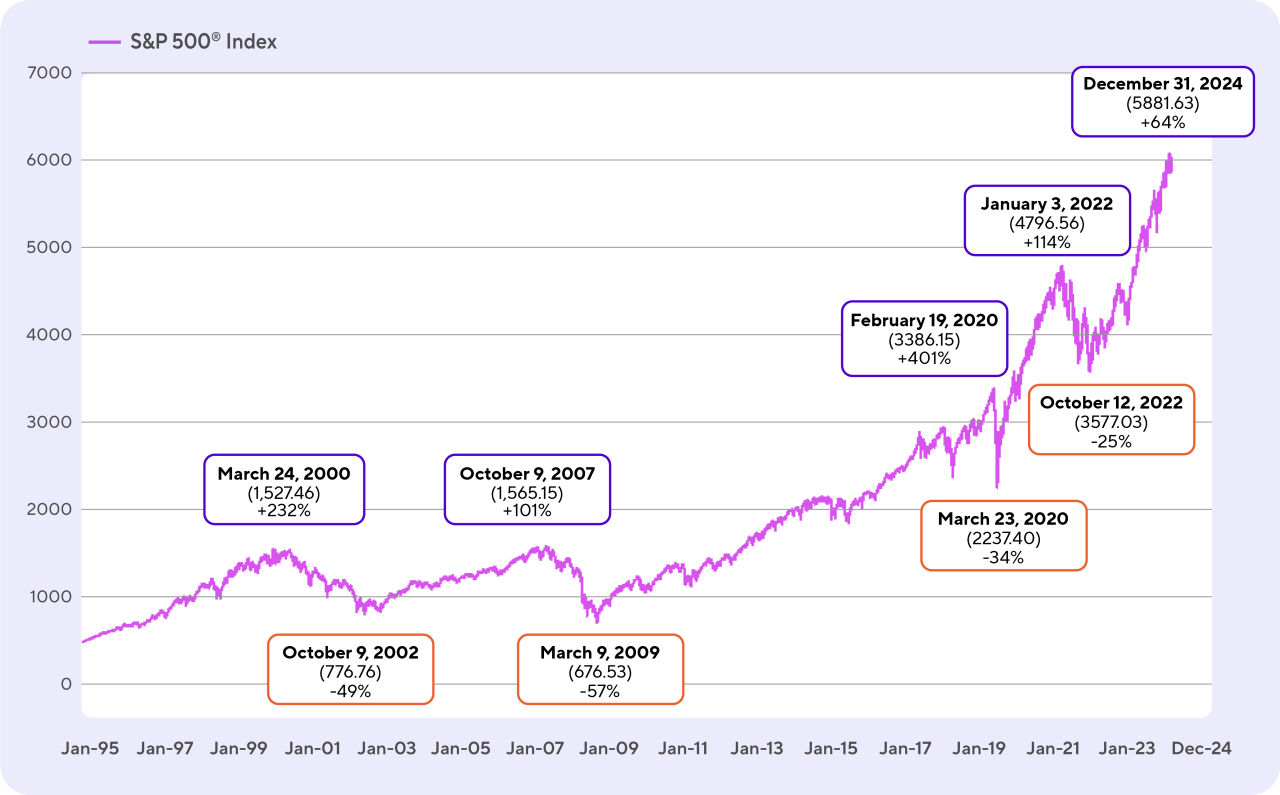

When saving for a long-term financial goal, such as retirement, you may want to consider the long-term growth potential of stocks. Over the past few decades, the stock market (as shown and represented below by the S&P 500® Index) advanced from a level of 459.11 at the beginning of January 1995 to reach a level of 5881.63 at the end of December 2024. That’s more than a tenfold increase over this 30-year period. Of course, past performance is not indicative of future results. And you should also remember that an investment in stocks is subject to market risk, including possible loss.

While the long-term trend of the stock market has been positive, there have been many ups and downs along the way, including a number of significant market downturns. For example:

- The 2008-2009 Global Financial Crisis brought with it a 57% price decline as of March 9, 2009.

- More recently, in the wake of the COVID-19 pandemic, stocks slid 34% from their prior high, with the S&P 500 Index closing at 2237.40 on March 23, 2020.

Investing in stocks often calls for a long-term perspective, along with patience and discipline.

This chart shows the long-term performance of the stock market, as represented by the S&P 500 Index. The chart begins on January 3, 1995 with an adjusted daily closing price of 459.11. It ends on December 31, 2024 with an adjusted daily closing price of 5881.63.

Planning for your financial future with stocks

As you think about stocks, and stock-oriented investments, and the role they may play in your overall retirement portfolio, here are a few key points to keep in mind based on your life stage:

- Early career: By taking action and investing in stock-oriented investments early in your career—perhaps through a workplace retirement plan, such as a 401(k) or 403(b)—you put time on your side. A longer time horizon can help you weather market ups and downs that may come along.

- Mid-career: As your career advances, you’ll likely be making more money. This may be an opportune time to save and invest even more for your future. For example, you may want to increase your contributions to a workplace retirement plan, if you have one, or start working with a financial professional to help build supplemental retirement savings.

- Late-career/pre-retirement: As retirement nears, it may make sense to talk with your financial professional about potentially dialing back risk in your portfolio, including stock exposure. When you’re in the later years of your career and retirement is fast approaching, you have less time to make up for market losses that you may encounter.

- Early retirement/retirement: Once you start drawing income from your retirement portfolio, the order in which you encounter positive or negative investment returns—known as the “sequence of returns”—poses a retirement risk that needs to be considered. Experiencing a market downturn in the early years of your retirement can increase the possibility of eventually running out of money. To help manage this risk, you may want to talk to your financial professional about an annuity with an income benefit, which can offer you protected lifetime income—no matter how the stock market performs.

Stocks and stock-oriented investments can play an important role in your overall retirement portfolio as you save and invest for your financial future, but they do come with risk. That’s why it’s important to work with a financial professional. A financial professional can help you navigate market ups and downs and help stay on track to meet your long-term financial goals.

Talk with a financial professional to design a retirement savings and income strategy that makes sense for you.

Annuities are long-term products designed for retirement. Early withdrawals may be subject to withdrawal charges. Partial withdrawals reduce the contract value and may also reduce certain benefits under the contract, such as the death benefit and the amount available upon a full surrender. Withdrawals of taxable amounts are subject to ordinary income tax and, if taken prior to age 59½, an additional 10% federal tax may apply. Guarantees are backed by the claims-paying ability of the issuing insurance company.

An investment in a variable annuity or registered index-linked annuity involves investment risk, including possible loss of principal. The contract, when surrendered, may be worth more or less than the total amount invested.

Annuity income benefits may be standard or optional. Additional fees, age restrictions and limitations apply. With variable annuities, investment requirements may also apply. Depending on investment performance and income needs, you may not need to rely on the protection provided by an income benefit. As an alternative to electing an income benefit, you can annuitize your contract and receive income payments for life at no additional cost.