When you reach your RMD age, you are required to withdraw at least a certain amount of your savings each year from your pretax retirement accounts and pay the taxes, even if you don’t need the money. RMDs can impact your taxable income and financial planning, so it’s important to understand what’s required and plan ahead. Some of the rules for RMDs changed with the SECURE 2.0 Act, so let’s look at what you need to know.1

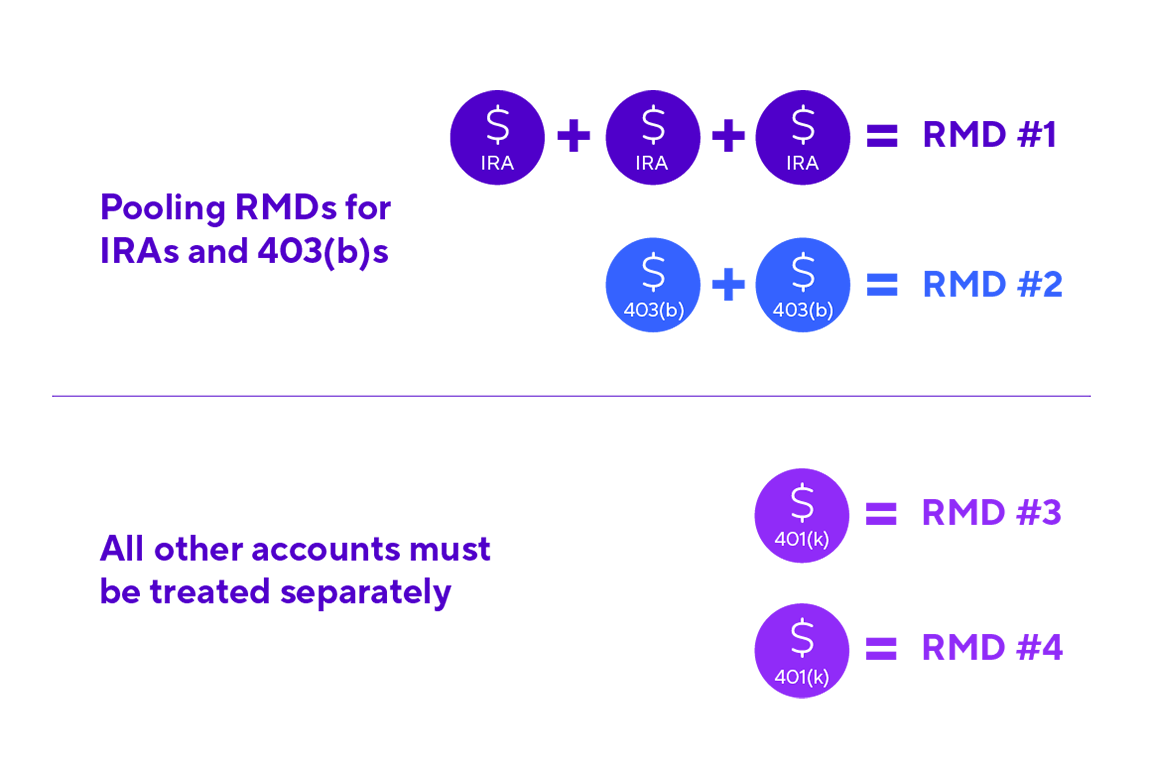

If you have an employer-sponsored retirement plan like a 401(k), 403(b) or 457(b), you’ll need to take RMDs on your pretax savings. If you own a traditional IRA, SEP IRA or SIMPLE IRA, you also must take RMDs. You do not have to take RMDs on Roth IRAs, since contributions were made after taxes were paid. And as of 2024, you also do not have to take RMDs on Roth accounts within an employer-sponsored retirement plan.

If you have not yet started taking RMDs, they will begin in the year you turn 73. You have until April 1 of the year after you turn 73 to take the first full RMD. After that, RMDs must be taken by December 31 each year. If you turned 72 in or prior to 2022, you should already be taking RMDs. In 2033 the RMD age will rise to 75.

Although first-time RMDs don’t have to be taken until April 1 of the year after you reach your RMD age, keep in mind that if you take your RMDs after December 31 of the year you turn 73 (that is, between January 1 and April 1 the following year), your second RMD must still be taken by December 31 of the same year. This could increase the taxes you might owe on the RMD by pushing you into a higher tax bracket. Check to see if this might affect you.