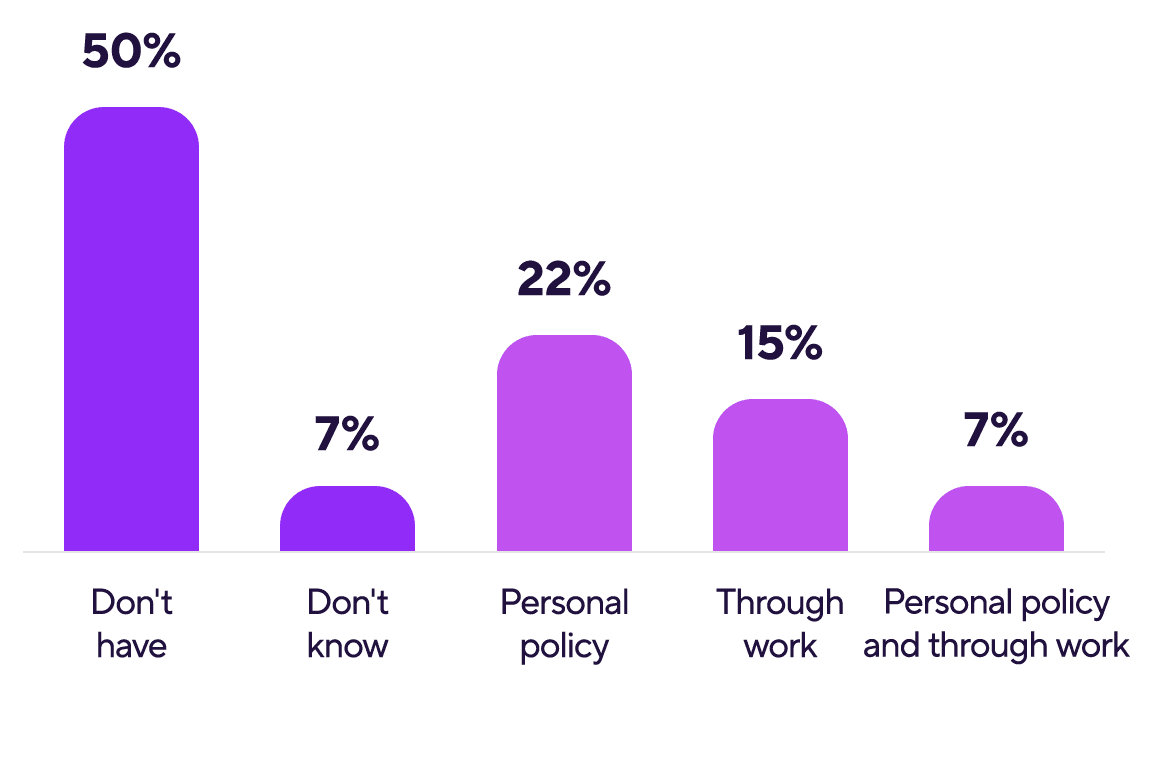

Many Americans are under or uninsured, with only 44% saying they have any coverage at all, according to Corebridge Financial’s 2025 Study, Understanding Life Insurance Needs. This and other findings from the survey of 2,200 Americans age 18+ provide valuable insights on how well consumers understand their coverage needs, what they consider the primary benefits of life insurance, their motivation to purchase coverage, and some of the perceived barriers.

The good news? There is a clear opportunity to improve consumer awareness of both the affordability of life insurance and how quickly individuals can get coverage. Financial professionals can play a pivotal role in helping educate Americans by addressing common misconceptions that life insurance is costly, complex, and difficult to obtain.

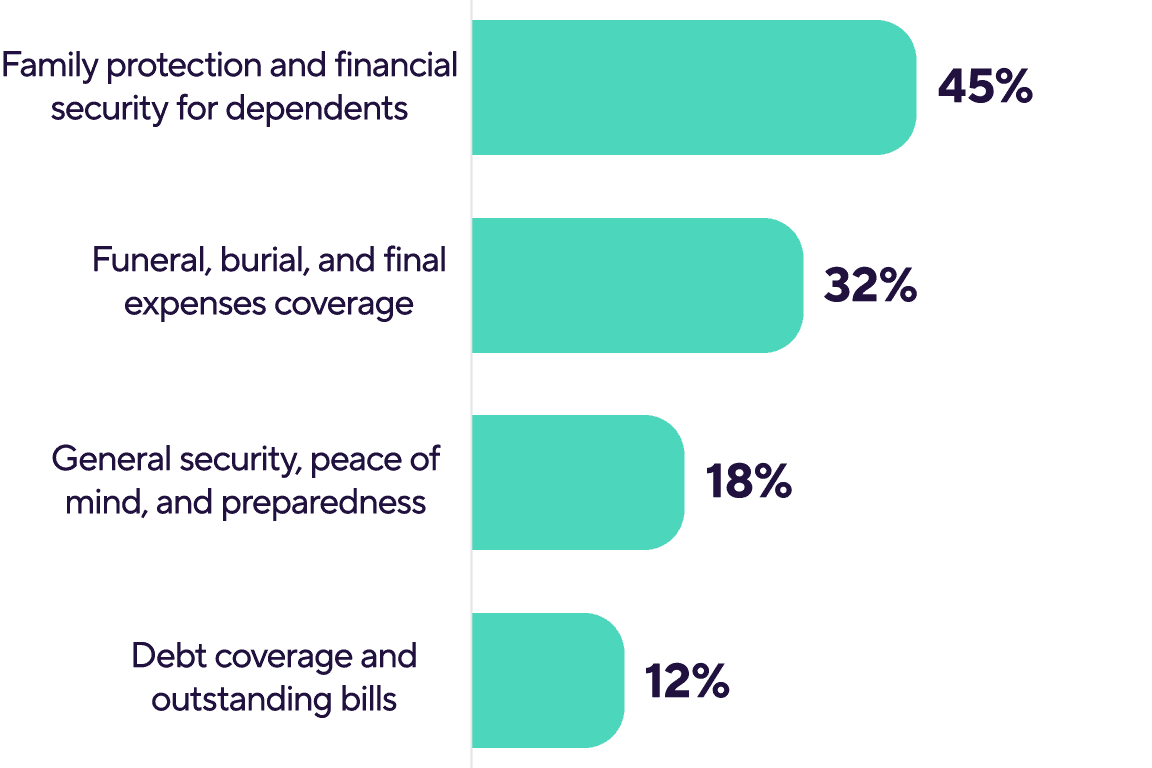

Key takeaways from the research include:

- Life insurance owners are more confident in their family’s ability to manage financially without them.

- A streamlined approval process and quick policy issue are incentives to get coverage.

- People say the expense is a barrier – but many are overestimating the cost of life insurance.

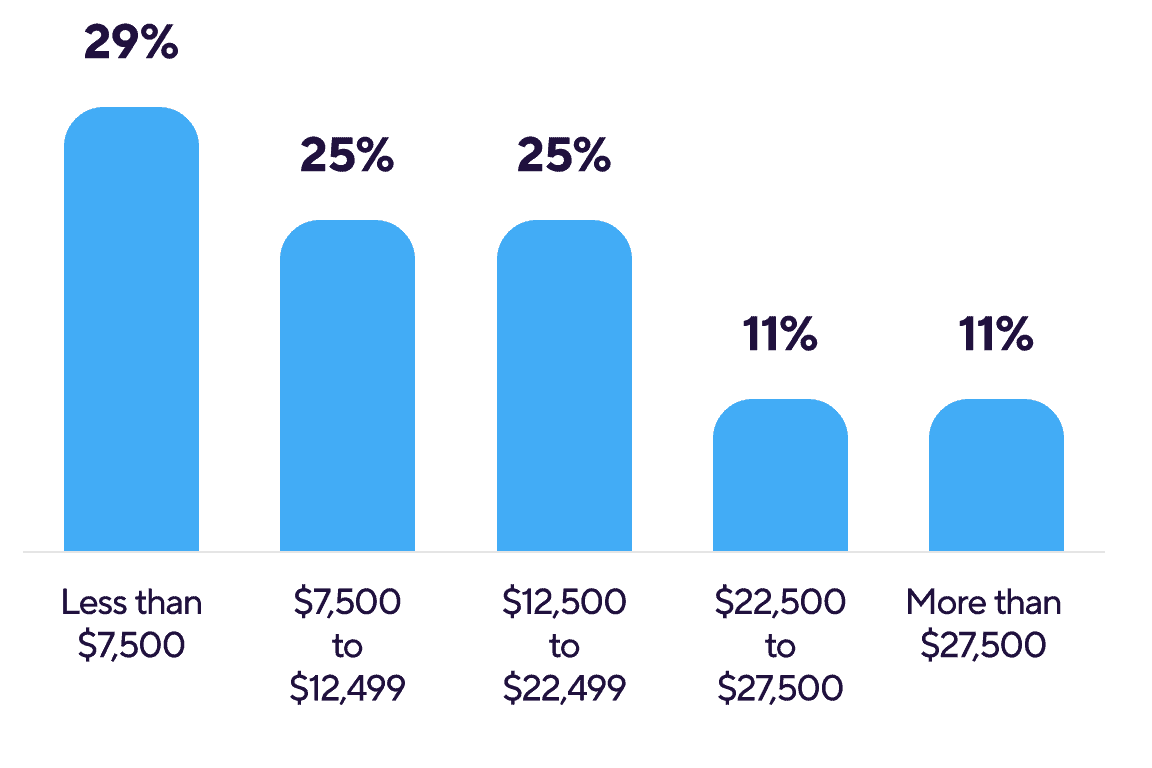

- While some have estimated end-of-life expenses, many are off target.

Life insurance builds confidence and is there to provide loved ones with financial support when it’s needed the most. That helps explain why Americans with life insurance compared to those without life insurance are more likely to be completely or very confident in their dependents’ ability to manage financially should they pass away (47% vs. 28%).