Auto-enrollment and auto-escalation are widely recognized as excellent strategies for improving plan participation and savings habits, but the full potential of these features is best realized when they’re combined with a robust communication and education plan.

Employers who offer a workplace retirement plan play a big role helping Americans save for the future. But providing access to a plan—although a great step—is just a starting point for driving financial wellness. Next level plans utilize auto features to get employees to start saving and follow up with a robust education plan to ensure they continue to take smart financial steps.

The role of auto features

Auto-enrollment

Auto-enrollment eliminates the need for individuals to actively opt into the plan, increasing the potential for improved participation rates and outcomes.

Auto-enrollment simplifies the decision-making process for employees by automatically enrolling them into their employer’s retirement plan at a predetermined contribution rate (unless they’re already enrolled or opt-out).

Although it may seem like employees are giving up control of their finances, auto-enroll provides the opportunity to decide—the only difference is that they must decide to not participate instead of deciding to participate. This is important considering many individuals don’t take action to enroll in their retirement plan because of a lack of understanding or fear.

While employees benefit from this simple way to begin saving for the future, auto-enrollment also has clear advantages for plan sponsors:

- It can streamline the new employee onboarding process.

- A higher percentage of employees save for retirement, which can help improve the overall financial wellness of the workforce.

Case Study

Auto-enrollment has proven to be an effective solution for boosting participation and plan assets

Corebridge recently partnered with a plan sponsor who had a participation rate that stood at just 26 percent in 2020. Additionally, plan assets were not nearly as high as they should have been for a plan with close to 4,700 participants.

The plan sponsor took a three-step approach to improve their plan:

- Selected Corebridge as the single provider

- Added auto-enrollment for new hires

- Offered one-time open enrollment for all employees

The results

- Enrollment jumped from 26 percent to 92.5 percent

- Total contributions increased from $206,000 to $969,000

SOURCE: Corebridge Financial. “Increased engagement = improved participant outcomes” December 2022.

Even though automatic enrollment drives employees into the plan, one of the key considerations when thinking about implementing the approach is the default contribution rate, which often defaults participants to a conservative option which is often too low for sufficient long-term retirement savings. This highlights the importance of also implementing auto-escalation to help ensure participants increase their contribution rate as time passes.

Auto-escalation can further drive employee financial wellness

Auto-escalation helps address barriers to saving by ensuring participants steadily contribute more over time.

Auto-escalation works in tandem with auto-enrollment by increasing an employee’s contribution rate over time, until it reaches a preset cap—helping them easily and gradually save more without requiring them to make active decisions.

This simplification is important because many employees are reluctant to increase their contribution rate due to competing financial priorities, inertia, or lack of knowledge about how much they need to save. Setting the annual escalation date on the same date as when employees get annual raises is a best practice.

The benefits of education and guidance

While auto features are powerful tools to help participants start moving in the right direction with little effort, retirement plans that pair these features with clear education can help employees achieve improved outcomes.

For plan sponsors, this reinforces the importance of working with a plan provider who can deliver a comprehensive communication and education plan that individuals can understand and act on. The following features are essential:

- A clear and informative participant website simplifies enrollment while delivering important educational and financial literacy content.

- Interactive digital resources such as planning calculators, budget trackers, retirement income estimators and others allow employees to model different scenarios and outcomes.

- Online articles and content help participants understand relevant current issues, including how they can navigate uncertainties such as inflation, market volatility, and longevity risk, and benefit from key financial strategies like compounding, diversification and dollar-cost averaging.

- An expert webinar series available live and on demand can provide insight on financial basics like compound interest and the power of saving early, determining contribution amounts, understanding investments, managing student loan debt, retirement readiness, wealth transfer, and more.

- Personalized recommendations. Mine your plan data to uncover where participants may need more specific communications. For example, younger employees may benefit from information on the power of compound interest, while older employees may need guidance on catch-up contributions and retirement readiness.

- Access to professional financial advice. Providing access to financial professionals through your plan provider can help grow employee confidence in their ability to successfully navigate their financial lives. In fact, those who work with a professional report much higher levels of financial confidence.

Consider the challenges before implementation

When implementing an automatic enrollment and escalation program, plan sponsors should carefully consider potential challenges—like the ones below—and weigh them in the light of how partnering with an experienced provider can help overcome them:

- Administrative burden—Proper oversight is necessary to guarantee that all eligible participants are timely enrolled and escalation amounts are accurately aligned with payroll withholdings.

- Plan document amendments—The program will likely require updates to plan documents to accommodate the auto features.

- Financial impact on employers—As participation grows due to automatic enrollment, plan sponsors who make matching contributions may experience a financial impact.

- Financial hardship for employees—If automatic escalation absorbs too much of employees’ annual pay, the potential financial hardship could lead participants to opt out of the plan, take out plan loans, or apply for hardship withdrawals.

- False sense of security for participants—Plans that select a smaller contribution amount for participants—at or around 1 percent—need to ensure these individuals periodically review their accounts to make sure this lower contribution percentage is adequate to help them reach their long-term financial goals.

Auto-enrollment and auto-escalation are tools that can help enhance the retirement readiness of plan participants. However, the full potential of auto-features is realized when they are combined with a robust communication and education plan.

For plan sponsors, investing in these automatic features and coupling them with a strategic, ongoing communication effort can lead to better retirement outcomes for employees, while also creating an environment where employees feel both supported and informed.

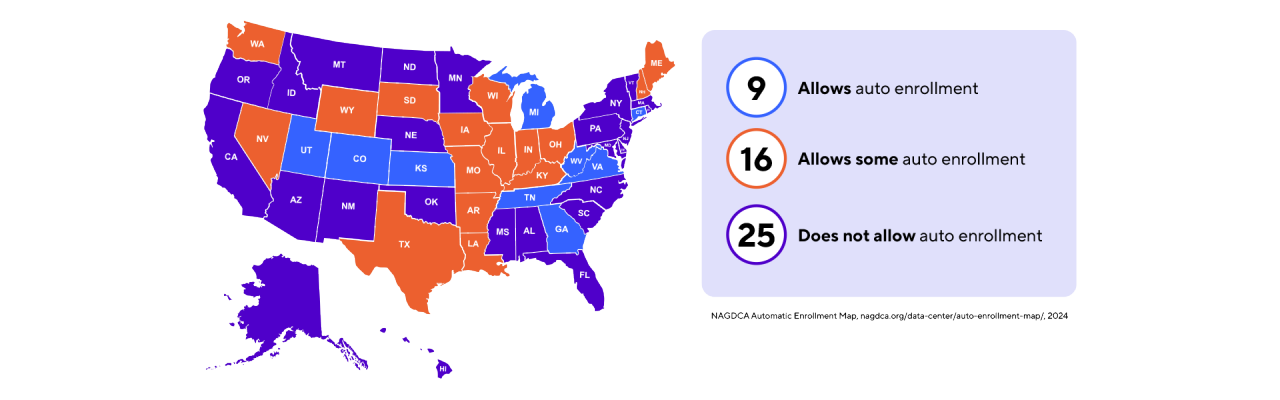

Are automatic options allowed in your state?

Colorado

Connecticut

Georgia

Kansas

Michigan

Tennessee

Utah

Virginia

West Virginia

Arkansas

Illinois

Indiana

Iowa

Kentucky

Louisiana

Maine

Missouri

Nevada

New Hampshire

Ohio

South Dakota

Texas

Washington

Wisconsin

Wyoming

Alabama

Alaska

Arizona

California

Delaware

Florida

Hawaii

Idaho

Maryland

Massachusetts

Minnesota

Mississippi

Montana

Nebraska

New Jersey

New Mexico

New York

North Carolina

North Dakota

Oklahoma

Oregon

Pennsylvania

Rhode Island

South Carolina

Vermont

At Corebridge, we believe that great things can happen when people take action.

Action is everything.

We’re committed to helping individuals actively plan and prepare for retirement through the resources, tools and solutions we offer—and through the financial professionals and institutions we proudly partner with.

1 Corebridge Financial Survey of Public Sector Workers, November 2023 with Morning Consult.

2 NAGDA Automatic Enrollment Map, nagdca.org/data-center/auto-enrollment-map/, 2024