Talk to a financial professional at no additional cost

Get help with enrollment or a plan for saving.

Get the Corebridge app for on-the-go access to your account

![]()

![]()

1 Income taxes must be paid at withdrawal. Federal restrictions and a 10% federal early withdrawal tax penalty may apply to withdrawals prior to age 59½.

2 This example is hypothetical and assumes a 25% federal marginal income tax bracket. Income taxes must be paid at withdrawal. Bear in mind that investing involves risk, including possible loss of principal.

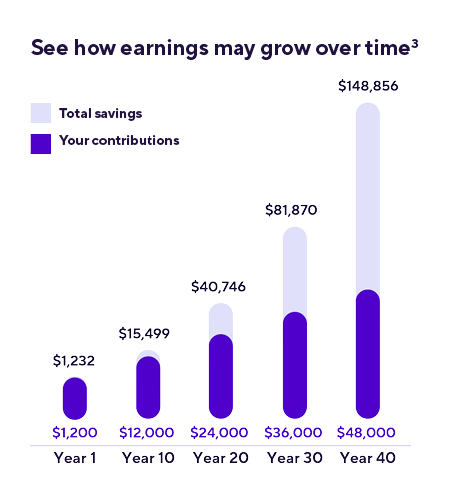

3 This example is hypothetical, does not reflect the return of any specific investment, and is not a guarantee of a specific rate of return. Figures are based on an annual 5% rate of return on monthly contributions of $100. Income taxes must be paid at withdrawal. Federal restrictions and a 10% federal early withdrawal tax penalty may apply to withdrawals prior to age 59½. Investment return and principal value will fluctuate so that the investor’s units, when redeemed, may be worth more or less than their original cost. Fees and charges, if applicable, are not reflected in this example and would reduce the results shown. Bear in mind that investing involves risk, including possible loss of principal.

RO 4474549 (05/2025)