The cost of borrowing from your retirement account

When planning for your financial future, it's crucial to account for those little expenses that sometimes blindside you - like medical expenses or car repairs. Sometimes those little expenses turn into big expenses and you need a little more to cover the cost. Maybe you want to buy a house and need a large chunk of change for a down payment. Perhaps you lost your job and need some cash to cover expenses until you can get back on your feet. It can be tempting - if you need a lot of cash - to look at all the money in your retirement plan for a low interest loan. But before you decide to dip into your account, there are a few things you should know.

"Retirement accounts were created to help you save money over a long period of time to use when you retire. Taking the money out before then can affect how much you'll have later on."

Take a loan...

Retirement accounts were created to help you save money over a long period of time to use when you retire. Taking the money out before then can affect how much you'll have later on. There are basically two ways you can get money out of your employer-sponsored retirement savings plan – take a loan, or withdraw the funds. If your plan allows for tax-free loans, you can access your account – subject to certain conditions – without permanently reducing your account balance. For example, if your balance is $100,000 and you borrow $40,000, you are left with a balance of $60,000. With a loan, you make payments, with interest, to return to your previous balance.

… or make a withdrawal?

On the other hand, if you make a withdrawal, you are not required to return that amount to your plan. It does automatically get taxed, and you could also be charged a 10% federal early withdrawal penalty if you're under the age of 59 ½. But let's take a look at the biggest reason to think long and hard before you decide you absolutely need to take some funds out of your retirement savings.

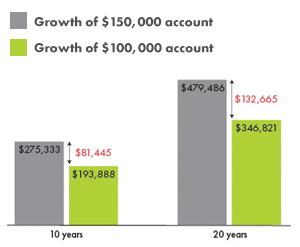

The long-term effect

Stephen withdrew $50,000 from his retirement plan, which at the time had a balance of $150,000. The withdrawal reduced the balance to $100,000. Stephen decided he needed the money immediately, and that it wouldn't be a problem later. But take a look at the long-term impact.

These charts compare the hypothetical results of contributing $200 each month for 10 years to a $150,000 account versus a $100,000 account. The example assumes a 5% annual rate of return, the federal marginal income tax rate of return. The federal marginal income tax rate and fees and charges, if applicable, are not reflected in this example and would affect the results shown. Income taxes are payable on withdrawal, and federal restrictions and tax penalties apply to early withdrawals. This information is hypothetical, only an example, does not reflect the return of any investment, and is not a guarantee of future income.

Chart that shows the effects of a $100,000 investment that had $50,000 borrowed from it. After 10 years, $81,445 was lost and after 20 years, $132,665 was lost.

In this hypothetical example, you can see the impact that withdrawals from your retirement savings can have. At the end of 10 years, Stephen's retirement account – minus the $50,000 withdrawal – grew to $193,888. If he had not taken the withdrawal, the account would have been worth $275,333 – $81,445 more! And after 20 years, the difference is even greater.

Withdrawing money from your retirement account reduces your assets in your portfolio and your potential earnings. It can also have long-term consequences.

- Withdrawing money from your plan could increase the risk of running out of money during retirement.

- Withdrawals are subject to ordinary income tax. Federal restrictions and a tax penalty might apply to early withdrawals.

Decisions regarding loans and withdrawals are important now and for your long-term goals. Your financial professional can assist you in evaluating these options. Financial advice is offered through VALIC Financial Advisors, Inc.

This information is general in nature, may be subject to change, and does not constitute legal, tax or accounting advice from any company, its employees, financial professionals or other representatives. Applicable laws and regulations are complex and subject to change. Any tax statements in this material are not intended to suggest the avoidance of U.S. federal, state or local tax penalties. For advice concerning your situation, consult your professional attorney, tax advisor or accountant.

This message may contain confidential, proprietary or legally privileged information and is intended only for the person or entity named above. No confidentiality or privilege is waived or lost by any mistransmission. If you are not the intended recipient of this message, you are hereby notified that you must not use or disseminate it, copy it in any form or take any other action in reliance on it. If you have received this message in error, please delete it.

To ensure compliance with requirements imposed by U.S. Treasury Regulations, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.