Plan for the phases of retirement

Managing your nest egg isn’t one distinctive event – it’s an ongoing process that needs to reflect life’s changes throughout retirement.

Many people look forward to retirement with a mix of pride, anticipation and a little angst/trepidation. After working hard and saving for so many years, it’s time to relax and enjoy the fruit of all that labor—but with retirement comes some very real concerns that include the potential for expenses to shift/grow as you age, the rising cost of healthcare and managing your income/stretching your savings over a 30- or 35-year period.

Understanding how costs will evolve over the course of your retirement can help you plan for your long-term needs. To put these concerns in context, consider retirement as a series of phases rather than one continuum.

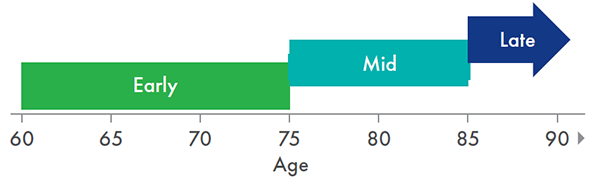

Let’s visually make this a spectrum.

- Early retirement from the 60s to mid-70s

- Mid-retirement from the mid-70s to early/mid-80s

- Late retirement from the mid-80s to the end of your life

To build the retirement you deserve, each phase requires its own financial strategy.

Early retirement

In early retirement, most people are full of renewed energy and eager to explore new opportunities. You’re free to explore your passions, hobbies, travel and indulge yourself in areas that you previously didn’t have time for due to your career. You may also find yourself helping to support adult children, assisting elderly parents or contributing to your grandchild’s education.

It comes as no surprise that many people find this time to be the most expensive stage of their retirement. They’re caught between wanting to enjoy their newfound freedoms and needing to ensure they don’t burn through their savings. Balancing your need for growth in investments with guaranteed income is critical during this stage.

Middle retirement

About 10 to 15 years into retirement, retirees tend to be settled into their new lives and some are considering downsizing their house or going to a single car. For others, this is the time to move closer to friends and family or choose a retirement community. At this stage, healthcare spending begins to increase, so it’s important to consider additional expenses for health or mobility in your income plan.

Late retirement

By the time you reach late retirement, the situation changes yet again. Many retirees in this stage enjoy sticking closer to home, so the travel portion of the budget declines. Healthcare issues move to the front burner. These can get expensive, which is why planning for long-term care expenses is an important part of retirement planning. Also consider setting up a power of attorney with a trusted financial professional, attorney or family member who can make financial decisions on your behalf if you are unable to do so. If you haven’t done this yet or need to revise your plan, consult with your attorney or financial professional.

Managing your income

There’s a common theme running through these stages – balancing your income with your expenses. Throughout retirement your income will likely derive from three sources:

- A pension or pension-like income

- Social Security

- Income from investments

As your income needs and the market environment shift, you need to ensure the income and growth components to your retirement income plan continue to function as you expected when you created the plan with your financial professional. Your Social Security and other guaranteed income will remain stable throughout retirement, but at each stage you should assess your investments to make sure your income strategy is in line with your projected expenses and guaranteed income options.

While you need a growth component to your investments, the need for guaranteed income is important as well. You don’t want a sudden change in the market to wipe out your savings and impact your ability to meet your income needs. This is where a source of guaranteed income or pension-like income can protect you from the fluctuations of the markets so that you can meet your financial obligations regardless of how the market is performing.

Partner with a trusted financial professional

There are predictable events at most stages of retirement, which financial professionals experienced in retirement income distribution can help you anticipate. Such an individual can help you build an income strategy based on your particular situation that offers additional sources of guaranteed income.

A financial professional can also review your retirement portfolio and make suggestions to ensure your income strategy covers at least your essential expenses throughout a 30- or 35-year retirement.

However you decide to spend your retirement, the key is to keep a pulse on your anticipated expenses and income so that you’re prepared for all the changes that come with a rewarding retirement.